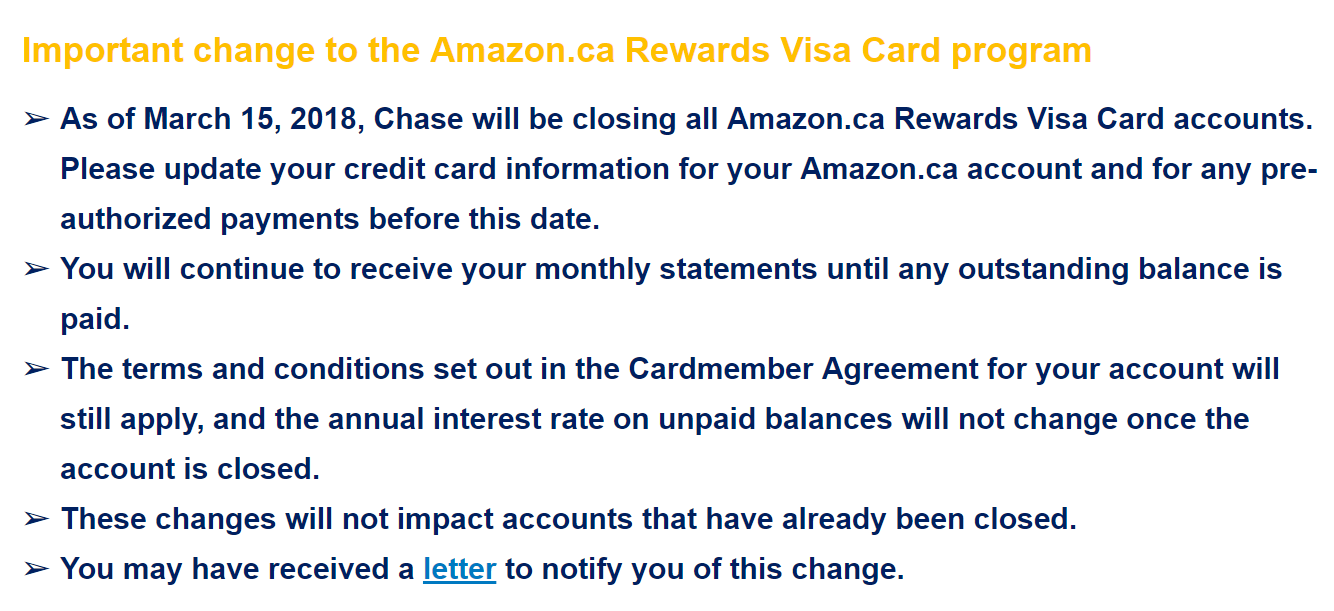

Chase Canada Closing All Amazon.ca Credit Cards March 15

Update (Jan 15, 2018): Chase will also close all Marriott Visa cards in Canada on March 15, 2018.

Chase Canada has been leaving the consumer credit market, having sold most of their portfolio to Scotiabank and ending applications for the Marriott Rewards and Amazon.ca credit cards. Unfortunately, as of March 15, 2018, all Amazon.ca credit cards will be closed.

Considering Chase no longer accepts applications for any credit products in Canada, I think it’s only a matter of time until Marriott accounts are also closed.

The Amazon.ca credit card was fantastic, giving you 1% cash-back and no foreign exchange fees (compared to the 2-2.5% charged by most banks). While there are new entrants to the market with similar benefits (Rogers/Fido MasterCard/Home Trust Visa), the Amazon.ca card was by far the most flexible and easy to use.

If you hold the Amazon.ca card, I would recommend proactively closing your account prior to March 15, 2018. If the bank closes your account, it will likely show on your credit bureau as “closed by creditor.” If you close it proactively, it will show as “closed by consumer.”

Goodnight, sweet prince. You’ll be missed.

End of an era. It was my really good no frills card. Now it looks like I have to apply to Rogers or Fido 🙁

I just called Chase Canada and learned that the Marriott Visa cards are also being cancelled on the same date – March 15th. I’m leaving for Europe in a couple of weeks so this is really annoying being given such short notice. I’ll need to scramble to find an alternative.

What happens if you have outstanding reward point but has not reached $20 yet?

The statement says you will receive an account credit.

The notice said, “upon closure of our Marriott Rewards Visa Card account you will be awarded your anniversary Free Night…” If we call to close the account ourselves, do we still get the free night or is the free night only after they close it?

Should I actually cancel the card myself? I’ve never seen this written before and always let the company close the account. Seems silly that it would negatively affect my credit score if they’re the ones deciding to close the account.

Anyone have any suggestions for a Canadian credit card that does not have a foreign exchange fee?

I wondered this too, and I’m not a Rogers customer, so their $29-a-year Platinum Mastercard didn’t appeal to me at first, but then a friend pointed out that in the fine print it says you can have the points credited to your account in January, as long as you call before December 1st. Not bad considering you get 1.75% back on all purchases. There is technically a 2.5%foreign fee, but you get 4% back on foreign purchases, meaning you’d actually be getting 1.5% back. You’d pay the yearly fee after spending $1,700 on it at 1.75% back.

The other option is the Home Trust Preferred Visa. $0 fee, 1% back on everything, no foreign conversion fee. You also get roadside assistance included, but only 5km local towing. You also get credited in January, so out of the two, the Rogers one is more appealing to me.

Fido Mastercard is better, exactly the same benefits as Rogers Mastercard (as long as you call before December 1st to withdraw your cashback) minus the $29 annual fee

I withdraw my comment, there is a slight difference in the cashback rate of Canadian purchases (1.75% for Rogers, 1.5% for Fido). However, paying $29 for it is only worth it if you plan to spend more than $11 600 per year on this card for purchases in Canadian currency. (0.25% * $29 = $11 600). The foreign currency rate is the same.

Yes I did notice that. Thank you for the Fido tip! I think I just may do that.

I fail to see why letting Chase close the account should have a negative impact on one’s credit rating. We’ve been through this before when they pulled out of Sears. I assume they will now be out of the credit card business in Canada entirely. Good riddance! I would never trust them again anyway.

No it won’t affect your credit, it will update to “Closed by Grantor” or “Account Cancelled/Non-Derogatory” on your credit report. Both statuses won’t affect your credit.

Any potential lender would interpret your credit history in their own way – if a note that an account was closed by the creditor indicate something negative in their view, this could affect your chances of getting approved for whatever it may be. Credit reports are terrible in this sense, you never get an opportunity to explain any of the information on it and businesses need to be effective and quick in their decisions, basically they just need to assess the risk you pose to their bottom-line, and they don’t have to take any unnecessary risks or often they will cover themselves by charging higher interest or applying other monetary overages to your agreement with them. It all depends on how the rest of your credit history look, in the eyes of the beholder.

If you close the card before the 15th, you will not get the cash back you have accumulated. If you close the account, it will be forfeited.

Wow, good point. Thank you

“If you hold the Amazon.ca card, I would recommend proactively closing your account prior to March 15, 2018. If the bank closes your account, it will likely show on your credit bureau as “closed by creditor.” If you close it proactively, it will show as “closed by consumer.””

Thanks very much for this!

• As of March 15, 2018, you will no longer be able to use your card for new transactions.

This is what the first bullet point of the Jan. 15, 2018, notification letter says. Further down the letter is says, “If you have a rewards balance at the time your account is closed, you will receive a statement credit for the full amount of your rewards balance.” How are you supposed to use the statement credit if the account is closed and you cannot use it for new transactions? Do we have to request a credit balance refund check?

The first bullet point of the Jan. 15, 2018, notification letter says.”As of March 15, 2018, you will no longer be able to use your card for new transactions.” Further down the letter is says, “If you have a rewards balance at the time your account is closed, you will receive a statement credit for the full amount of your rewards balance.” How are you supposed to use the statement credit if the account is closed and you cannot use it for new transactions? Do we have to request a credit balance refund check?

“I would recommend proactively closing your account prior to March 15, 2018” would qualify as the worst advice of the decade – whoever did this didn’t receive the final closing certificate for one night at a category 1-5 hotel.

News of the certificate came after this article

Hello to every , since I am genuinely keen of reading

this web site’s post to be updated on a regular basis. It contains good information.